Claims denials in U.S. health insurance pose a serious problem for patients navigating their care. In this report we present and analyze data that sheds light on the occurrence and prevalence of claims denials in commercial health insurance, propose policies to improve patient outcomes, and highlight existing avenues for consumer recourse. Our analyses show that commercial claims denials correspond to a highly valuable population of claims, and that even modest improvements to appeal access, utilization and outcomes have the potential to return billions of dollars to consumers.

Table of Contents

- Introduction

- Transparency Statement

- Acknowledgments

- A Primer on Claims Denials

- Denials

- Appeals

- Public Claims Denial Data

- Overview

- Datasets

- Submitted Claims and Denials

- Internal Appeals

- External Appeals

- Conclusions

- Lack of Evaluation of Commercial Internal Appeal Processes

- Monetary Value of Appeals

- Need for Data Standardization, Validation and Enhancement

- Need for Standardization and Streamlining of Appeals Processes

- Recommendations

- Policy

- Patient Recourse

- Cite This Work

- BibTex

- Plain Text

- References

Introduction

Claims are a fundamental and atomic unit of U.S. health insurance: every time an insured consumer attempts to use their health insurance to cover a portion of a bill, a claim is submitted to their insurer on their behalf. The claim records details about the care received and its cost necessary for an insurer to make a payment determination. The primary role of health insurers is to receive and adjudicate these claims based on the contracts they sell, and ultimately pay for some portion of them, on behalf of those who purchased the contracts (typically employers or individuals).

When insurers adjudicate a claim to determine whether they will pay for it, they review the contracts that govern the coverage which has been purchased on behalf of the insured. The permissible content in these contracts is often restricted by laws and regulations, and the contracts may also refer to external sources (e.g. "clinical policy bulletins", or "scientific literature") which will be used to inform coverage determinations. We will say a coverage decision is contractually inappropriate if the decision is inconsistent with the contract governing a policy, or the laws and regulations that apply to that policy.

There are many coverage decisions that one might deem morally or medically inappropriate that would not be considered contractually inappropriate. For example, it would be morally troubling for corporations to sell policies that exclude the coverage of expensive treatments for those facing dire medical situations in such a way that the relevant contract clauses conflate actual scientific consensus with consensus according to a for-profit corporation’s own non-expert reading of their hand picked literature selection. However, such behavior is not necessarily contractually inappropriate.

Contractually inappropriate claims denials, and the lack of adequate recourse for consumers even in these cases, have been serious problems for a long time. There are organizations that regularly publish reports analyzing the limited publicly available claims denial data (Pollitz & Rae, 2020), and the subject has been discussed in policy research, legal research (Fox, 2022) and popular journalism (Konrad, 2010) for a long time.

Recently, there have been numerous investigations and articles that have brought to light for the general public just how damaging some of the inappropriate practices taking place really are (Armstrong et al., 2023b, 2023a), and illuminated the scarcity of publicly available data (Fields, 2023).

Finally, there are those most seriously affected; many patients with dire, serious, or chronic medical needs (and their friends and families) have long known about the lack of recourse they enjoy, and the frequency with which contractually inappropriate denials occur just in seeking their own care -- they have been on the front lines for decades, suffering the consequences of an inadequately regulated industry.

In this work, we set out to illuminate the extent and prevalence of claims denials, and the crucial monetary role they play in our systems. To do so, we analyze publicly available claims denial and appeal data. We seek to do this analysis in a transparent, and reproducible way, to ensure that our work can be extended and used by others seeking to improve patient outcomes, justice, and accountability. We discuss this more explicitly in our transparency statement below. It is our hope that the analyses in this report can be used to catalyze change, such as in supporting those seeking to convince decision makers to enact relevant policy.

Transparency Statement

We aim to publish reports in such a way that all of our analyses, plots, and numerical claims drawn from data can be vetted, reproduced, and built upon as desired. We believe the ability to reproduce results end to end is crucially relevant in discussions of this topic, as existing data and transparency are scarce and poorly understood, and there are many conflicting voices and viewpoints in the space.

To this end, we provide transparent, open source access to all analyses and data used to generate this document. The interested reader may probe any aspect of our end to end analyses of raw data provided by government institutions by investigating the following resources:

All non-interactive figures appearing in this report, as well as the data populating interactive figures, were generated via the code housed here.

Data we obtained via public records is hosted here.

A static copy of this entire article is housed here.

If you believe there are errors in this report, analytical or otherwise, we would appreciate your correspondence. Our goal is to achieve rigorous results that can be audited by anyone, and that constitute trustworthy evidence that improves in quality over time. We hope to build trust with you by providing such open access to our end to end workflow.

To correspond about our analyses, please open an issue in our public repository, or send us a message at info@persius.org.

Acknowledgments

It is a pleasure to thank the following people for their support in editing and improving this work:

Alan Bush, Ph.D.

For editorial and organizational support.

To be clear, despite their contributions to this article, the parties above do not necessarily share views expressed, nor does their editorial support constitute endorsement of opinion.

A Primer on Claims Denials

A claim denial occurs when a claim is submitted to an insurer, and the insurer decides they will not pay for it. In practice, such decisions are made for many reasons; some valid1, and others inappropriate or indefensible.

When a claim is denied, a patient is typically left with an out of pocket expense larger than what they would otherwise face.

Denials

One of the most basic metrics that one can use to investigate how claims handling varies is an overall claims denial rate. This measures the fraction all claims submitted that are denied:

This is not a uniquely defined notion, because the numerator and denominator can be defined in various ways. For example, one could compute this ratio for all claims submitted to a particular insurer over the course of a year, or for all of the claims submitted for a particular plan over a month, or even for all claims submitted from just one individual to a given plan over the course of a year2. In what follows, we will calculate denial rates that fit this form in a few different ways.

It is worth noting that:

- Among the claims that are appropriate3, a low denial rate is always a good thing for patients.

- High denial rates can be caused by numerous things, and do not necessarily indicate inappropriate insurer practices.

Appeals

When insurers deny claims, patients are often entitled to an appeals process. For example, those with federal marketplace plans are afforded such recourse, as are all others with so-called non-grandfathered commercial qualified health plans (see (Pollitz, 2021) for more background); Medicare allows for its own distinct processes for appealing denied claims; and Medicaid programs support their own distinct processes (see e.g. this guide).

The details of these processes vary based on details of one's insurance plan and relevant regulations, but typically they allow patients to initially file an internal appeal of the denial, which is adjudicated by the insurer itself. This is the case, for example, in commercial insurance plans, which are the primary focus of this article given the data we analyze.

If the internal appeal process (which in some plans requires an insured to make two attempts at an internal appeal) results in the insurer upholding their denial, patients are then sometimes able to file an external appeal. This means they can submit an appeal of the decision to a independent third party that is responsible for judging the merits of the determination; the final determinations of these third parties are typically binding. The third parties, and processes by which external appeals are submitted to them and reviewed by them, vary according to the details of the type of plan involved.

In understanding the landscape of claims denials, it is useful to understand the frequency of occurrence, and distribution of outcomes, of these internal appeal processes.

Internal Appeal Rates

We define the initial internal appeal rate to be the fraction of denied claims that are appealed at the first (internal) level available to consumers.

Again, this is a loose definition that we will specify more precisely in each particular calculation below.

Of those denials that are internally appealed, we denote the fraction that are overturned by the insurer as the internal appeal overturn rate.

External Appeal Rates

We define the external appeal rate to be the fraction of denials eligible for external appeal (this consists mostly of internally appealed and subsequently upheld denials) which are actually externally appealed by consumers.

Of those denials that are externally appealed, we denote the fraction that are overturned by a third party as the external appeal overturn rate.

Public Claims Denial Data

Overview

To understand the landscape of claims denials, contractually inappropriate claims denials, appeals, and effective consumer recourse, we need data. Unfortunately, requirements for commercial insurers to publicly disclose claims denial data are few and far between, and the extent to which requirements that do exist are enforced and regulated is unclear. However, some publicly available data does exist.

Datasets

We make use of the following publicly available data:

Federal Marketplace Public Use Files (PUFs) from the Centers for Medicare and Medicaid Services (CMS)

Dataset Details

Each year CMS releases a collection of transparency data related to federal marketplace insurers. Here we are interested in the transparency in coverage4 (TIC) public use files. These are files compiled from self-reported insurer data specifying aggregate counts of claims submitted, claims denied, and claims appealed, among other things. This data is limited in scope, but it is the closest thing we have to a denial transparency survey among commercial plans with broad (geographical) scope. It is compiled and reported to the public in accordance with the Department of Health and Human Services (HHS) rule 45 of the Code of Federal Regulations (CFR), part 155, subpart K, (cf CFR 156 subpart C).

In this article we focus on the 2023 public use file, which details claims denial data from the 2021 plan year.

This 2021 data corresponds to:

- Plan year 2021.

- 33 states.

- 230 unique insurers.

- 6,764 plans.

- 8,251,703 consumers.

New York Health Care Claim Reports

Dataset Details

Thanks to legislation from 2020, New York publishes health care claim reports for insurance companies that contain aggregate counts of claims submitted, claims denied, and claims appealed for each commercial NY insurer, among other things.

This data, released quarterly as of 2022 in the form of spreadsheets for each New York insurer, details aspects of health insurance coverage for insurance plans in New York. Various details about how the data is reported are included in the frequently asked questions for the data on the DFS homepage.

Residents of New York state can not buy individual Affordable Care Act (ACA) compliant Qualified Health Plans (QHPs) on the federal marketplace. Instead, NY maintains its own marketplace where such plans can be purchased, known as New York State of Health. The New York Health Care Claims Reports includes statistics relating to NY marketplace plans, in addition to plans that are not sold via the marketplace.

In this article, we analyze the health care claims report data from 2022. The 2022 data includes:

- Plan year 2022.

- 29 unique insurers.

- 145,446,802 claims adjudicated, worth at least $66,810,881,848.

- 25,996,601 claims denied, worth at least $2,265,844,512.

- 177,917 claims denied for medical necessity, worth at least $35,747,594.

- 145,129 internal appeals adjudicated, worth at least $303,942,639.

- 42,375 overturned internal appeals, worth at least $124,245,612.

All denials recorded in the data are post-service claims denials, so pre-authorization denials are not included. Appeals in the data include both appeals submitted directly by consumers, and appeals submitted by providers on behalf of consumers.

New York External Appeal Outcome Data

Dataset Details

External appeals of denials from New York marketplace plans, fully insured group plans, and Medicaid managed care plans are adjudicated by Independent Review Organizations. The New York Department of Financial Services maintains a public database of results from such external appeals.

The New York External Appeal Database corresponds to:

- Plan years 2019 to 2023.

- 24,728 external appeals.

- Individual and group health plans.

- Fully insured employer plans.

- IMRs associated with plans regulated by the New York State Department of Financial Services.

In this article we discard the subset of the dataset corresponding to claims from 2023; such claims correspond to an incomplete plan year, and they have the potential to introduce confounding inconsistencies into our analyses. We initially included them in our analyses, but found they led to easily misinterpreted results.

Washington External Appeal Outcome Data

Dataset Details

In Washington state, claims denial data is not generally made public. However, as in New York, the final adjudication status of claims which are both ultimately externally appealed and fall under the authority of the Office of the Insurance Commissioner (OIC) are recorded in a publicly accessible dataset.

External appeals of denials from Washington marketplace plans are adjudicated by Independent Review Organizations. According to Washington Administrative Code 284-43-3030 and the Revised Code of Washington 48.43.530, insurers must support both internal and external appeal processes, and report resulting data to the insurance commissioner. The code above provides for external appeals to be sought as soon as an internal process is exhausted, or 30 days after internal appeal initiation has occurred, whichever is sooner. Details of the rules pertaining to external appeals are described in the Revised Code of Washington 48.43.535.

The OIC in Washington state maintains the aforementioned public database of results from these external appeals. This data corresponds to consumers enrolled in Washington health plans that are regulated by the Office of the Insurance Commissioner (OIC). This includes, but is not limited to, individual plans sold on the Washington marketplace (known as Washington Health Plan Finder).

The OIC external appeal database corresponds to:

- Plan years 2016 through 2023.

- 8,774 external appeals

- Individual and group health plans.

- Self insured and fully insured employer plans.

- IMRs associated with plans regulated by the OIC.

In this article we discard the subset of the dataset corresponding to claims from 2023; such claims correspond to an incomplete plan year, and they have the potential to introduce confounding inconsistencies into our analyses. We initially included them in our analyses, but found they led to easily misinterpreted results.

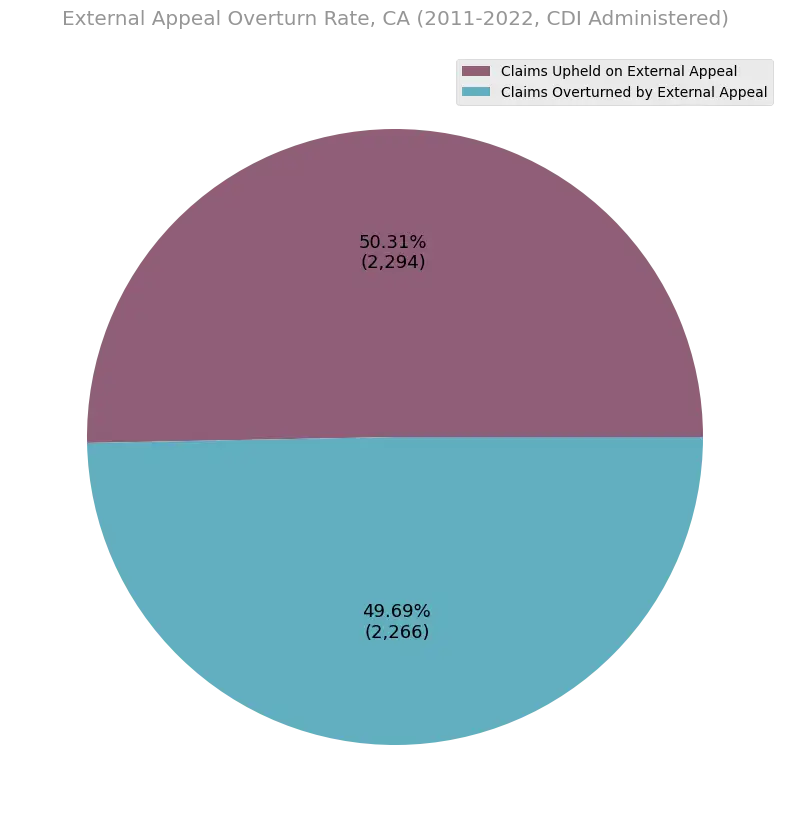

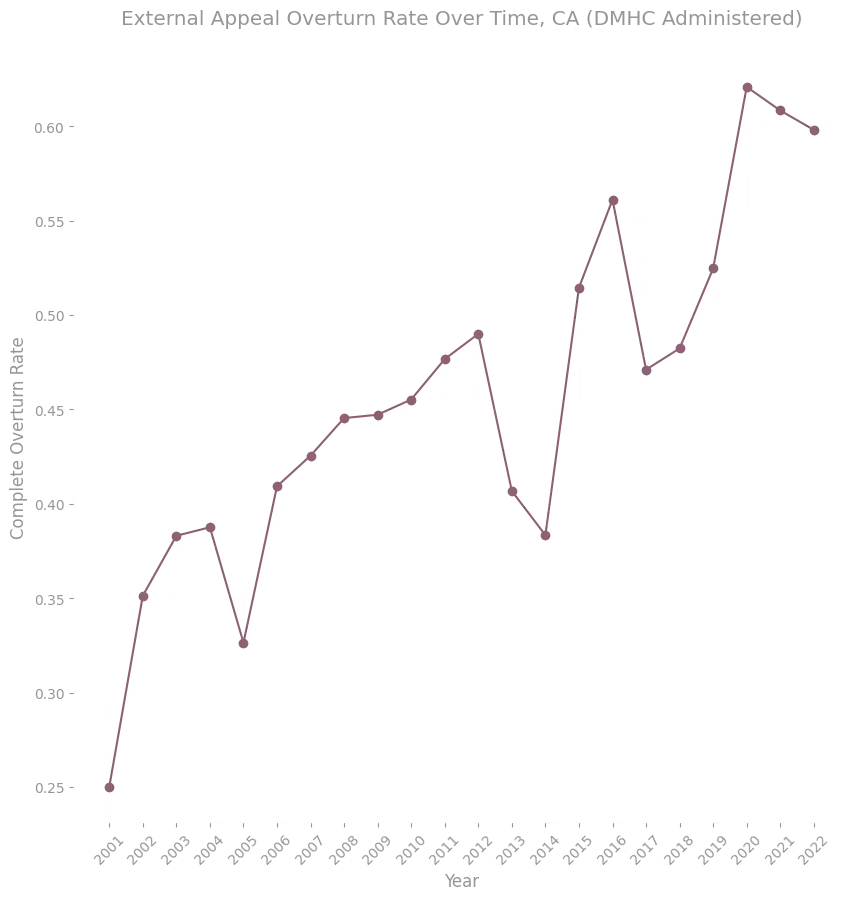

California External Appeal Data from the California Department of Insurance (CDI) and the Department of Managed Health Care (DMHC)

Dataset Details

California releases data related to internal and external appeal outcomes in at least four places, all of which we consider:

- Yearly CDI commissioner reports.

- These reports include summary statistics, such as the total numbers of claims and internal appeals submitted by consumers. The specific yearly reports we consider here are released by commissioner Ricardo Lara.

- Yearly DMHC secretary reports.

- These reports include summary statistics, such as the total numbers of claims and internal appeals submitted by consumers. The specific yearly reports we consider here are released by director Mary Watanabe.

- A database of Internal Medical Review (IMR) outcomes regulated by the California Department of Insurance.

- This data corresponds to plans regulated by the CDI.

- A database of Internal Medical Review (IMR) outcomes pertaining to health maintenance organizations (HMOs).

- This data corresponds to plans regulated by the California Department of Managed Health Care (DMHC).

External appeals in California, also known as Independent Medical Reviews (IMRs), follow processes dictated by two pieces of the California Insurance Code (CIC).

- Sections 10169.1 - 10169.5, which initially became effective January 1, 2001, describe rules that apply to IMR sought for health coverage decisions purportedly related to medical necessity. There have been numerous modifications to the law since then. The current law expressly provides for the inclusion of those on Medicare and Medicare Advantage plans, however it also allows for processes to be subsumed by existing state Medicare resolution outlets. It allows IMRs to be sought as soon as an internal process is exhausted, or 30 days after internal initiation has occurred, whichever is sooner. It also allows the CDI to contract with the DMHC to administer the IMR as desired (which has come into play for managed care plans, such as HMOs, as described in the last dataset description above.)

- Section 10145.3, also effective as of January 1, 2001, describes particular rules that apply to IMR sought for insurer decisions stemming from deeming treatment or services as experimental or investigational in nature.

The CDI IMR database corresponds to:

- Plan years 2011 through 2023.

- 4,719 Independent Medical Reviews.

- Individual and group health plans.

- Self insured and fully insured employer plans.

- IMRs associated with plans regulated by the California Department of Insurance.

The DMHC IMR database corresponds to:

- Plan years 2001 through 2023.

- 34,615 Independent Medical Reviews.

- Individual and group health plans.

- Self insured and fully insured employer plans.

- IMRs associated with plans regulated by the California Department of Managed Healthcare.

In this article we discard the subset of both datasets corresponding to claims from 2023; such claims correspond to an incomplete plan year, and they have the potential to introduce confounding inconsistencies into our analyses. We initially included them in our analyses, but found they led to easily misinterpreted results.

- Yearly CDI commissioner reports.

Connecticut Denial Data From Consumer Report Cards

Dataset Details

Each year Connecticut's Department of Insurance releases a report, the so called Consumer Report Card on Health Insurance Carriers. The report includes various aggregate statistics about health insurance plans, including utilization for certain services, member satisfaction, and aggregate denial statistics.

The yearly data is released as a published PDF report, and corresponds to all insurance plans sold by Connecticut issuers except those that are government sponsored; in other words, all CT health insurance enrollees other than those with government sponsored plans (e.g. Medicaid and Medicare plans) are represented. As such, the data pertains to both individual and group health insurance plans, including self insured and fully insured employer plans.

In this article we focus on the 2022 report, which details claims from the 2021 plan year.

The data corresponds to coverage for:

- Plan year 2021.

- 11 unique insurers.

- 1,991,903 consumers.

- HMO and indemnity plans.

- Individual, small group and large group plans.

- Self insured and fully insured plans.

Pennsylvania Department of Insurance claims denial data (New Data Release)5

Dataset Details

Pennsylvania utilized the federal marketplace for qualified health plans until the end of 2020, when it transitioned to using its own newly formed marketplace, known as Pennie, in accordance with the passage of PA House Bill 3. Beginning in 2021, consumers could buy qualified health plans on the Pennsylvania marketplace.

We submitted a public records request under the Pennsylvania Right to Know Law to the Pennsylvania Insurance Department (PA DOI) asking for a comprehensive analysis of various aggregate statistics pertaining to claims adjudication for which we believed they were likely to have records. This dataset is the result of that request. While the data is not as comprehensive or extensive as we had hoped might be possible, it is a step forward. We are releasing the raw data we obtained, as well as parsed and preprocessed adaptations of it, to the public along with the release of this article.

The dataset contains aggregate counts for claims, denials, and internal and external appeals broken down by issuer for claims corresponding to marketplace plans, plus an undisclosed additional population of plans, from plan years 2020 and 2021. In addition, the data includes claims, denials and denial rationales broken down by plan for the subset of claims corresponding specifically to marketplace plans (this subset constitutes a large majority of the dataset to begin with).

The data obtained from the PA Department of Insurance corresponds to:

- Plan years 2020 and 2021.

- 13 unique insurers.

- 599 unique plans.

- At least 337,722 consumers.

- 21,646,696 claims adjudicated

- 2,964,421 claims denials.

- 2,751 internal appeals.

- 103 external appeals.

- Individual marketplace plans.

- Possibly additional group plans regulated by the PA Department of Insurance.

An overview of the data we analyze in this report is detailed below.

| Data Source (plan years considered) | Market Segment Represented | Number of Denials | Denial Levels Represented | Consumer Population Represented |

|---|---|---|---|---|

| CMS TIC PUF (2021) | Federal marketplace | 48,302,001 | All | 8,251,703 |

| NY Health Care Claims Reports (2022) | All commercial, Medicaid managed care, Essential Plan, and Child Health Plus plans | 25,996,601 | All | Unknown, but > 5,000,000 6 |

| NY External Appeals Database (2019-2022) | NY marketplace, fully insured group plans, and Medicaid managed care plans | 24,728 | Externally Appealed (IMR) | Unknown, but > 5,000,000 6 |

| WA External Appeals Database (2016-2022) | WA marketplace | 8,774 | Externally Appealed (IMR) | 222,731 |

| CA DOI External Appeals Database (2011-2022) | CA marketplace, and fully insured group plans | 4,719 | Externally Appealed (IMR) | 852,506 7 |

| CA DMHC External Appeals Database (2001-2022) | Large group and self funded plans regulated by DMHC | 34,615 | Externally Appealed (IMR) | 23,474,332 8 |

| Connecticut Consumer Report Card (2021) | All CT issuers (excluding government sponsored) | 2,708,724 | All | 1,991,9039 |

| Pennsylvania Department of Insurance Data (2020, 2021) | PA marketplace plans, plus some subset of Department of Insurance regulated group plans | 2,964,421 | All | Unknown, but > 337,722 10 |

To our knowledge, this is the first report that compiles aggregate results across a wide array of disparate sources containing claims denial data from different market segments, and the first public report to analyze claims denial data from the Pennsylvania marketplace. The varied nature of the data makes it difficult to make direct comparisons across datasets, but we believe it is still informative to witness the extent to which certain phenomenology occurs consistently across these datasets, despite the varied contexts and regulatory settings in which the data is produced.

Although we collect and analyze data from many sources, the data is far from complete, even among any fixed market segment such as federal and state ACA exchanges.

We note that we submitted many public records requests seeking data that would allow us to perform a more comprehensive account of all marketplace claims denial data. However, with the exception of Pennsylvania, the state insurance departments to which we submitted requests were unable or unwilling to grant our requests.

The state departments of insurance which did not grant our requests either cited lack of access to such data, or claimed that our (admittedly non-expert) reading of the Department of Health and Human Services (HHS) rule 45 of the Code of Federal Regulations (CFR), part 155, subpart K, (cf CFR 156 subpart C), which suggests to us both that

- ACA exchange claims denial data must be made available to the public for all ACA exchanges.

- Each state's department of insurance should have access to that data.

is incorrect.

Our interpretation, which of course may be flawed, comes from the following chain of logic:

- CFR part 155, subpart K, § 155.1040 (a) suggests "The Exchange" must collect transparency data in accordance with CFR part 156, subpart C (specifically § 156.220).

- CFR part 156, subpart C (specifically § 156.220) suggests that such claims denial data must be furnished by QHP issuers to both exchanges and state insurance commissioners, and that such data must include the number of claims that are denied (by § 156.220 (b) and § 156.220 (a).(5) respectively).

- CFR part 156, subpart C (specifically § 156.220 (b)) suggests that some entity must make that data available to the public.

- "The Exchange" in CFR part 155, subpart K seems to be referring to any exchange (whether federal or state run) based on CFR part 155, subpart A specifically, so the points above should apply to all state exchanges, in addition to healthcare.gov.

In at least one case, a response from a state department of insurance to our records request claimed that the CFR sections cited above do not require the State to collect denial data. We do not yet understand a reading of the CFR text that allows for this interpretation.

In addition to failing to gain access to claims denial data for some state marketplaces, we also simply neglected to consider some data that is already public; we did so only for expediency, not lack of interest or relevance. For example, we have not yet incorporated claims denial data made available by Covered California, but plan to incorporate such data into a subsequent iterate of this article in the near future.

Finally, we note that the total number of unique consumers represented across all of the data sets we consider is unknown (see the Consumer Population Represented column in the data summary table above). However, what is clear is that this population is a small fraction of the total population of insured individuals in the U.S. This fact is not surprising, given that many of the datasets we consider correspond to data from highly limited market segments (e.g. individual plans sold on state marketplaces) which comprise a small fraction of all insurance plans. Having claims denial data for the entire population of the insured U.S. population would be invaluable for ensuring accountability and the ability to effectively audit the justness of adjudication processes at large; we make the case for the need for such data in our concluding policy recommendations section.

Submitted Claims and Denials

Four of the datasets we consider here provide information sufficient to compute overall initial denial rates in particular market segments, as well as denial rates broken down across subcategories of those market segments.

These datasets are:

- CMS TIC PUFs.

- New York Health Care Claims Reports.

- Connecticut Consumer Report Cards.

- Pennsylvania Department of Insurance Data.

In what follows, we attempt to provide common views of the disparate datasets to facilitate considerations about comparison when possible, but we warn the reader that direct comparisons should not assumed to be valid, as these datasets are reported according to inconsistent methodologies. In fact, we don't even have temporal overlap of the plan years reported for all of the datasets. For example, the NY Health Care Claims Reports have only been reported since plan year 2022, while the CMS TIC PUFs have been regularly published for many years, but have yet to be made public for plan year 2022.

Despite the inconsistencies in reporting, all of the data suggests that denials are generally prevalent, regardless of how one slices the data.

We will now walk through calculations of overall claims denial rates in each dataset that allows for such a calculation. We perform these broad, general calculations to serve as a background for all subsequent calculations, and provide context for the scale of the issues at play. After computing the overall denial rates, we will consider how denial rates break down in various ways: by denial associated denial rationale, by insurer, and by state or region, to name a few.

Overall Denial Rates

First we consider overall denial rates for each of the datasets.

CMS Federal Marketplace PUFsOn the federal marketplace, 16% of all claims submitted in 202111 were initially denied. This data is displayed in Figure 1.

Figure 1. Aggregate denial rate across federal marketplace insurers in 2021. Approximately 16% of all federal marketplace claims were initially denied in 2021, according to CMS TIC PUF data.

Source: CMS TIC PUF data.

Among New York insurers, 18% of all claims submitted in 2022 were initially denied. This data is displayed in Figure 2.

Figure 2. Overall denial rate (18%) among all NY issuers who submitted health care claims reports to the Department of Financial Services in 2022.

Source: NY Health Care Claims Reports.

Among Connecticut insurers, 25% of all claims submitted in 2021 were initially denied. This calculation involved throwing out seemingly spurious data reported for the indemnity plans for one insurer, Connecticare (the report indicates Connecticare had more denials of claims than actual claims received). This data is displayed in Figure 3.

Figure 3. Overall claims denial rate in CT consumer report card data.

Source: 2022 CT Consumer Report Card

Among Pennsylvania insurers represented in the PA DOI data, approximately 15% of all claims submitted in 2020 were initially denied, while approximately 13% of the claims submitted in 2021 were initially denied. This data is displayed in aggregate in Figure 4.

Figure 4. Overall claims denial rate in the Pennsylvania Department of Insurance data in in 2020 and 2021.

Denials By Rationale

When insurers deny coverage of a claim, they must report their rationale for the denial. The rationales, and the details of how they must be reported to both the insured and regulatory agencies, vary by plan, but typically include a small set of mutually exclusive labels. In each of the datasets that provide denial counts, some metadata regarding the denial rationales is included, though the details vary by dataset.

CMS Federal Marketplace PUFsFederal marketplace plans included in the CMS TIC PUF data sometimes report rationales for claim denials. Figure 5 shows the categories allowed in the CMS PUF reporting methodology, and their frequency of occurrence in the subset of data which includes rationales.

Most denials logged in the CMS PUF data are associated with a rationale of "Other". This provides little information about the underlying nature of the denials.

Figure 5. Distribution of claims denial rationales in a subset of the TIC PUF data. Denial rationales are reported at the plan level, and we only included here those plans which reported denial rationales which either summed to the total number of denials reported, or which summed to the total number of denials reported excluding out of network denials. For some plans, neither validation method held, and we could not resolve what standard was being used to report the rationale data; that rationale data is not included. Source: CMS TIC PUF data.

Effectively, this reporting scheme allows insurers to withhold reporting the actual reason for a denial to the public if they so choose, since it is not completely clear what is allowed to be reported in the "Other" bucket, and there is no strict validation of the reported data. Whether or not insurers actually abuse the system in this way cannot be gleaned from this data alone.

New York Health Care Claims ReportsThe New York Health Care Claims Reports detail the rationales for all of the denials documented in the data, but allow for a different set of available options for denial rationales. These rationales, and their relative frequency of occurrence within the data, are shown in Figure 6.

Figure 6. Distribution of denial rationales for all denials recorded in the health care claims reports submitted to the Department of Financial Services in 2022.

Source: NY Health Care Claims Reports.

Again, we see that an ambiguous "Other" category is utilized heavily in the reporting. Furthermore, while many of the rationale categories in this dataset are well-defined terms that have consistent, standard meaning across the industry (see e.g. a typical definition of step therapy), others are ambiguous.

For example, the "Not Covered or Limitation" label here is our abbreviation of a label specified in the raw data as "Not a covered benefit/Exceeds benefit limits (e.g., visit limits)", which is a broad category that appears to allow for many interpretations, similar to the "Other" category. It would be useful to understand more explicitly exactly which subset of denials are being recorded in the "Not Covered or Limitation" category, as opposed to the "Other" category, or the "NMN or Experimental" category, since there is ambiguity and conceptual overlap in each of these concepts. For example, claims deemed to be not medically necessary or experimental are typically a subset of services that are explicitly considered 'not covered', according to language in insurance contracts.

Connecticut Consumer Report CardsThe Connecticut consumer report cards detail rationales for every denial recorded in the data, but again use a different set of categories, and make liberal use of an "Other" category. The data is displayed in Figure 7.

Figure 7. Distribution of denial rationales for all denials in the CT consumer report card data. Source: 2022 CT Consumer Report Card.

The Pennsylvania Department of Insurance data details rationales only for denials recorded at the plan level in the data (which is the subset corresponding to marketplace claims), but the story remains the same in that the set of permissible rationales in the data is distinct from each other set we've considered. The data is displayed in Figure 8.

Figure 8. Distribution of denial rationales for all denials in the PA DOI data.

'Not Medically Necessary' Denial Rates

Each of the datasets considered provides a category of denial rationale corresponding to purported lack of medical necessity or experimental nature of a service (what we will collectively call NMN denials).

While NMN denials occur relatively infrequently, as Figures 5, 6, 7 and 8 show, they still correspond to a large population of claims in an absolute sense; just for the tiny fraction of all insurance plans covered by the data shown above, for a single plan year, there are more than 700k such claims. Furthermore, they are an important subset of denials in the sense that:

- Their contractual merit is typically subtle, because it typically involves contractual definitions that themselves reference things like clinical policy bulletins, scientific literature, medical standards, or other external data.

- The consequences for such denials can be perilous for patients relying on coverage of treatments for debilitating issues that they would not otherwise be able to afford. This can be true for other rationale categories as well, depending on the categories considered, but is not the case for all categories (e.g. duplicate claims).

For these reasons, we draw attention to aspects of the data pertaining specifically to NMN denials, when possible. Unfortunately, the data is often insufficient to allow much to be ascertained definitively about this subpopulation of denials.

One thing we can understand definitively about the subpopulation of NMN denials in these datasets is the rate at which they occur among all claims; these rates can be deduced by reconsidering Figures 5, 6, 7 and 8, but we make the rates explicit in the table below.

| Data Source (plan years considered) | NMN Denials | Claims Received With Rationale | NMN Denial Rate | |

|---|---|---|---|---|

| CMS TIC PUF (2021) | 520,140 | 13,157,832 | .0395 | |

| NY Health Care Claims Reports (2022) | 177,881 | 34,168,504 | .0052 | |

| Connecticut Consumer Report Card (2021) | 27,517 | 2,006,049 | .0137 | |

| Pennsylvania DOI Data (2020) | 104,396 | 10,451,280 | .0099 | |

| Pennsylvania DOI Data (2021) | 66,031 | 9,494,221 | .0069 |

Unsurprisingly we see that NMN denial rates are orders of magnitude smaller than overall denial rates; however, it is interesting to note that there is significant variation in the overall NMN denial rate across these datasets. One contributing factor is surely the lack of standardization in reporting methodologies, such as the variation in the set of denial rationales permissible in the reported data. It is unclear to what extent the actual denial rates relating to medical necessity would vary across these datasets if one were to correct for reporting inconsistencies.

Denials By Insurer

Each of the datasets reporting denials includes breakdowns of the claims received and claims denied by insurer. It is informative to understand how the aggregate denial rates and NMN denial rates vary by insurer within each dataset.

We note at the outset that while it is informative to understand how various distributions vary by insurer, there are many subtleties lurking behind such breakdowns, just as there were for denial rationales. For example, different insurers may have different distributions of plan network types (e.g. relative fraction of consumers on HMO, EPO, PPO, and POS plans), and as a result insurer denial differences might partially be a reflection of the differences in those plan type distributions. Or, alternatively, two insurers might have identical plan type distributions and administration practices, but have a different list of drugs for which they require prior-authorization, with one list containing some much more commonly utilized drugs. Given such subtleties which the data does not allow us to address, it is difficult to definitively understand the cause of the phenomenology we observe in differences across insurers.

In the same vein, the distribution across insurers of denials whose rationale specifically involves the experimental nature of a treatment, rather than another medical necessity rationale, could be influenced by many things, in addition to the raw counts of claims. In particular, one would expect that wealthy and renowned hospital systems conducting cutting edge research would be more likely than others to attempt truly experimental or novel services for their patients in need, and that such properties of a hospital are correlated with other properties, such as proximity to a major city and research center. As a result, health insurance companies with networks that overlap certain geographic areas, or that include certain hospitals, might receive a distribution of claims with a relatively high share that could be interpreted as involving experimental treatments, when compared to distributions received by other insurance companies. In such a context, it would be inappropriate to make an inference about how experimental claims denial processes vary by insurer from experimental claims denial rates alone.

As with all of the data we examine in this article, there are many subtleties that make it difficult to draw conclusions without more information. We make suggestions to address this troubling predicament in the concluding recommendations section.

CMS Federal Marketplace PUFsFigures 9, 10 and 11 show the overall claims counts, denial rates, and NMN denial rates for the 10 issuers in the CMS TIC PUF Federal Marketplace data with the highest claims volume.

Figure 9. Claims received for the 10 issuers with the largest number of claims adjudicated in the 2021 CMS TIC PUF data.

Source: CMS TIC PUF data.

Figure 10. Overall claims denial rates for the 10 issuers with the largest number of claims adjudicated in the 2021 CMS TIC PUF data.

Source: CMS TIC PUF data.

Figure 11. NMN (including experimental) denial rates for the 10 issuers with the largest number of claims adjudicated in the 2021 CMS TIC PUF data.

Source: CMS TIC PUF data.

Among the largest federal marketplace issuers of 2021, as measured by claims received, Blue Cross Blue Shield of South Carolina has an NMN denial rate roughly two to three orders of magnitude larger than the others. It is unclear what drives this phenomenon.

Figure 12 shows a heatmap displaying the distribution of denial rationales among these same highest volume insurers.

Figure 12. Distribution of denial rationales for the 10 issuers with the largest number of claims adjudicated in the 2021 CMS TIC PUF data. The color indicates the fraction of all denials for a given insurer that were coded with a particular rationale (i.e. rows sum to 1). Source: CMS TIC PUF data.

Figures 13, 14 and 15 show the overall claims counts, denial rates, and NMN denial rates for the 10 issuers in the New York Health Care Claims Reports data with the highest claims volume.

Figure 13. Claims received for the 10 issuers with the largest number of claims adjudicated in the 2022 Department of Financial Services claims report data.

Source: NY Health Care Claims Reports.

Figure 14. Overall claims denial rates for the 10 issuers with the largest number of claims adjudicated in the 2022 Department of Financial Services claims report data.

Source: NY Health Care Claims Reports.

Figure 15. NMN (including experimental) denial rates for the 10 issuers with the largest number of claims adjudicated in the 2022 Department of Financial Services claims report data.

Source: NY Health Care Claims Reports.

Figure 16 shows a heatmap displaying the distribution of denial rationales among these same highest volume insurers.

Figure 16. Distribution of denial rationales for the 10 issuers with the largest number of claims adjudicated in the 2022 Department of Financial Services claims report data. The color indicates the fraction of all denials for a given insurer that were coded with a particular rationale (i.e. rows sum to 1).

Source: NY Health Care Claims Reports.

Figures 17, 18 and 19 show the overall claims counts, denial rates, and NMN denial rates for the 10 issuers in the Connecticut Consumer Report Card data with the highest claims volume.

Figure 17. Claims received for all issuers in the CT consumer report card data.

Source: 2022 CT Consumer Report Card

Figure 18. Overall claims denial rates for all issuers in the CT consumer report card data.

Source: 2022 CT Consumer Report Card

Figure 19. NMN (including experimental) denial rates for all issuers in the CT consumer report card data.

Source: 2022 CT Consumer Report Card

Figure 18 shows odd and potentially spurious data that indicates one set of issuers, 'ConnectiCare Benefits' and 'ConnectiCare', have extremely high claims denial rates above 85%. We suspect this is a reporting error in the raw data, but we show it here because we cannot be sure of that fact. We were unable to find further information about this anomaly.

Figure 20 shows a heatmap displaying the distribution of denial rationales among these same highest volume insurers.

Figure 20. Distribution of denial rationales for all issuers in the CT consumer report card data. The color indicates the fraction of all denials for a given insurer that were coded with a particular rationale (i.e. rows sum to 1).

Source: 2022 CT Consumer Report Card

Figures 21, 22 and 23 show the overall claims counts, denial rates, and NMN denial rates for the 10 issuers in the Pennsylvania Department of Insurance Data data with the highest claims volume.

Figure 21. Claims received for all issuers in the PA DOI data.

Figure 22. Overall claims denial rates for all issuers in the PA DOI data.

Figure 23. NMN (including experimental) denial rates for all issuers in the PA DOI data.

Figure 24 shows a heatmap displaying the distribution of denial rationales among these same highest volume insurers.

Figure 24. Distribution of denial rationales for all issuers in the PA DOI data who report denial rationales. The color indicates the fraction of all denials for a given insurer that were coded with a particular rationale (i.e. rows sum to 1).

Dataset Specific Considerations

Since the datasets do not report claims and denial information in a standard or consistent way, there are many interesting considerations that can be made for only some of the datasets. Here we present dataset specific considerations relating to claims and denial distributions.

CMS Federal Marketplace PUFsThe CMS TIC PUFs provide many pieces of metadata associated with individual plans, and their corresponding aggregate claims data, that allow denials to be broken down across additional categories.

At a high level, we can calculate the overall denial rate for each issuer (an insurer's state specific entity), by calculating the ratio of all claims denied by that issuer, to the claims received by that issuer (across all their plans). Figure 25 shows the distribution of such issuer denial rates across issuers represented in the 2021 CMS TIC PUF data. The distribution is bimodal, with a large majority of issuers comprising a contingency with aggregate denial rates between 0% to 30%, and a small contingency of issuers maintaining aggregate denial rates between 35% to 50%. While we could compute such a distribution for the other datasets as well, the number of issuers involved is too small to infer much from the resulting distribution. Here, however, the distribution sheds some light on how denial rates vary by issuer.

Figure 25. Distribution of claims denial rates across federal marketplace issuers in 2021. Across issuers, denial rates vary from approximately 0% to 50%.

Source: CMS TIC PUF data.

Each plan reported in the data also has metadata associated with it. Figure 26 contains two interactive plots that show the distribution of individual plan denial rates, as a function of two properties of plans:

Plan administration and network type

Health insurance plans utilize different network and administration policy types, which dictate things like which providers are considered part of your plans preferred network, and how you must seek certain types of care and services (e.g. by obtaining referrals for specialist visits). Some common policy types include Exclusive Provider Organizations (EPOs), Health Maintenance Organizations (HMOs), Point of Service (POS), and Preferred Provider Organizations (PPOs).

Metal level

Federal marketplace plans are partitioned according to so-called plan categories, which are mostly named by metals. The categories are Catastrophic, Bronze, Bronze Expanded, Silver, Gold and Platinum. Generally, plans that fall into a more precious metal category have higher premiums, but cover a larger fraction of the cost of care when coverage kicks in. Catastrophic plans, as the name suggests, typically only provide coverage for catastrophic situations.

The data show that

- A larger fraction of EMO and HMO plans have denial rates between 30% to 50% than do PPO and POS plans.

- Only platinum level plans completely lack a contingent of 30% to 50% denial rate constituents.

Denial Rates by Plan Type, Federal Marketplace (2021)

Denial Rates by Metal Level, Federal Marketplace (2021)

Figure 26 (interactive). Distribution of claims denial rates broken down by plan types, and by plan metal levels. Click on a plan type or plan metal level to see the corresponding distribution of denial rates.

Source: CMS TIC PUF data.

Figure 27 shows the average issuer level claims denial rates for each state or region represented in the CMS TIC PUF data, as well as various statistics of the data within each region. For example, we display the number of issuers represented in each state, the total number of claims represented for each state, and the issuers with the highest claims denial rates in each state.

Denial Rates By Region, Federal Marketplace (2021)

Figure 27 (interactive). Claims denial rates and other data attributes broken down by region. Hover over regions for more detailed information.

Source: CMS TIC PUF data.

We also include a table summarizing the data included in this interactive plot:

Table View

| State or Region | Overall Denial Rate | Claims Received | Claims Denied | Number of Consumers Reported | Number of Insurers Reported |

|---|---|---|---|---|---|

| Alaska | 0.235 | 611313 | 143836 | 16707 | 2 |

| Alabama | 0.224 | 7657061 | 1716993 | 168717 | 2 |

| Arkansas | 0.185 | 15180958 | 2808497 | 59629 | 5 |

| Arizona | 0.192 | 3612118 | 694976 | 115409 | 6 |

| Florida | 0.131 | 75588407 | 9868686 | 1867568 | 10 |

| Georgia | 0.289 | 10825149 | 3127963 | 387441 | 6 |

| Hawaii | 0.244 | 486179 | 118578 | 16343 | 2 |

| Iowa | 0.149 | 2828360 | 421458 | 40699 | 3 |

| Illinois | 0.176 | 10755531 | 1893905 | 248363 | 7 |

| Indiana | 0.236 | 4233263 | 997114 | 91625 | 3 |

| Kansas | 0.135 | 2333613 | 314062 | 43716 | 5 |

| Louisiana | 0.151 | 5040194 | 761581 | 78236 | 4 |

| Michigan | 0.205 | 7783687 | 1599048 | 138398 | 8 |

| Missouri | 0.191 | 6173944 | 1182181 | 113034 | 8 |

| Mississippi | 0.381 | 1411877 | 537222 | 50769 | 2 |

| Montana | 0.096 | 1379424 | 132490 | 41233 | 3 |

| North Carolina | 0.125 | 26446640 | 3295778 | 284269 | 5 |

| North Dakota | 0.042 | 1873450 | 77936 | 21803 | 3 |

| Nebraska | 0.102 | 3305776 | 338692 | 48619 | 2 |

| New Hampshire | 0.184 | 1436531 | 264608 | 34360 | 3 |

| Ohio | 0.217 | 5795555 | 1255800 | 138349 | 10 |

| Oklahoma | 0.163 | 8986426 | 1461998 | 138695 | 4 |

| Oregon | 0.07 | 1999967 | 139605 | 111343 | 6 |

| South Carolina | 0.18 | 10502152 | 1885641 | 179317 | 3 |

| South Dakota | 0.057 | 776818 | 44532 | 25419 | 2 |

| Tennessee | 0.18 | 11196451 | 2011182 | 140672 | 6 |

| Texas | 0.204 | 35256067 | 7201165 | 591074 | 10 |

| Utah | 0.138 | 10086291 | 1391050 | 151905 | 6 |

| Virginia | 0.164 | 9224112 | 1508696 | 224605 | 9 |

| Wisconsin | 0.117 | 5952081 | 694105 | 128863 | 13 |

| West Virginia | 0.162 | 883377 | 143100 | 7069 | 2 |

| Wyoming | 0.128 | 1157244 | 148487 | 26777 | 2 |

Among this federal marketplace data, Mississippi stands out for having a uniquely high aggregate denial rate, with Texas, Alabama, Alaska, Georgia, Ohio, Indiana and Michigan forming a contingent with the next highest rates.

In many regions, a relatively small collection of issuers contribute a majority of the claims denied.

New York Health Care Claims ReportsThe New York Health Care Claims Reports provide a different set of metadata associated with individual insurers, and their corresponding aggregate claims data, that allow denials to be considered from different lenses. The claims reports also include information relating to the monetary value of claims, which we consider in more detail below.

The reports include information that details how claims, denials, and appeals are broken down across different provider categories. The categories specified in the data are:

- Hospital Inpatient

- Hospital Outpatient

- Other Facilities Inpatient

- Physicians

- Other Health Care Providers

- Pharmacy

- Other

Of note, the "Hospital Outpatient" category includes all claims submitted for emergency room services, and the "Other Facilities Inpatient" category includes all claims submitted for inpatient rehabilitation or skilled nursing facility services.

Figure 28 shows the overall claims counts occurring in the dataset for each category, while Figure 29 shows the overall claims denial rates in each category, aggregated over all insurers in the dataset.

Figure 28. Claims counts broken down by provider category, aggregated across all insurers who submitted health care claims reports to the Department of Financial Services in 2022.

Source: NY Health Care Claims Reports.

Figure 29. Denial counts broken down by provider category, aggregated across all insurers who submitted health care claims reports to the Department of Financial Services in 2022.

Source: NY Health Care Claims Reports.

The relative frequency of denials across these categories is somewhat consistent with the distribution of claims received across the categories, but denial rates vary from 10% to 30% across the categories.

We can also observe how NMN denials specifically are broken down by provider category. This is shown in Figure 30.

Figure 30. Total claims denied for medical necessity or experimental nature of a treatment, for each provider category, aggregated across all insurers who submitted health care claims reports to the Department of Financial Services in 2022.

Source: NY Health Care Claims Reports.

The New York Health Care Claims Reports are unique in that they also provide detailed breakdowns of the monetary value associated with many of the aspects of the data they report. Generally, the data reports the value of claims in various subcategories via two mechanisms:

Allowed Amounts

An allowed amount for a service under a given plan is the maximum monetary value that the insurance plan will pay for a covered service.

Billed Charges

A billed charge is the actual monetary value that a service provider charges a patient or insurer; this amount need not agree with the allowed amount for a plan.

Figure 31 shows the collective value of NMN denials in the dataset, as measured by the total allowed amounts. Allowed amounts for NY NMN denials accounted for over 35M USD in 2022.

Figure 31. Total allowed amounts for claims denied for medical necessity or experimental nature of a treatment, for each provider category, aggregated across all insurers who submitted health care claims reports to the Department of Financial Services in 2022.

Source: NY Health Care Claims Reports.

The distributions for both NMN denial counts and corresponding allowed amounts across provider categories look largely similar to those for all denials, with two notable exceptions.

- There are very few Pharmacy denials for medical necessity in this data. One contributing factor for this is that the NMN category in this data does not include denials requiring the use of step therapy. While this is a separate denial category in this data, the categories are similar in that they involve a determination about purportedly medically appropriate treatments. Another contributing factor to the relative scarcity of pharmacy NMN denials is the reporting methodology: pre-authorization denials are not included in this data, which is one context in which one would expect NMN pharmacy denials to be occurring.

- Among NMN denials, Hospital Outpatient allowed amounts far outweigh those of Hospital Inpatient, unlike in the distribution among denials of all types.

While there are likely many factors driving the latter result, it is worth noting that generally data suggests that hospital revenue share from outpatient procedures has been consistently increasing, with a large share of orthopedic and minor surgeries occurring in outpatient settings. Collectively, these trends to perform certain types of services and treatments more frequently in outpatient vs inpatient settings, coupled with the distribution of purported medical necessity of services within these disciplines, as dictated by insurers, might explain why NMN denials for outpatient services correspond to a high total allowed amount, relative to the inpatient NMN denials.

We can also consider the proportion of denials in each provider category that correspond to each denial rationale. Figure 32 shows a heatmap displaying these distributions.

Figure 32. Distribution of denial rationales for each provider category in the 2022 Department of Financial Services claims report data. The color indicates the fraction of all denials in a given provider category that were coded with a particular rationale (i.e. rows sum to 1).

Source: NY Health Care Claims Reports.

While it is difficult to extract detail about the distributions from Figure 32 given the prevalence of "Other" rationale reporting, some trends are noticeable. For example, among the Pharmacy denials in the dataset that are not recorded under the "Other" category, a large proportion are coded as denials related to non-covered or limited services.

Connecticut Consumer Report CardsThe Connecticut Consumer Report Cards provide a few types of information that are not present in the other datasets. Most notably for our purposes, the reports include detailed breakdowns of how claims counts and enrollment are split across different market segments, such as plan type, plan funding type, and insurer. We display a few statistics relating to enrollment in what follows.

All claims data in the consumer report corresponds to a certain population of consumers. Understanding that population is highly relevant, as it serves as an important denominator for considerations about the average impact of claims denials on each person. For example, one might be interested in understanding the average number of medical necessity claims denials received by an individual member of an insurance plan over the course of a year. This sort of calculation requires an understanding of not just raw claims and denial numbers, but also enrollment, associated with a plan.

As we noted previously, the entire dataset corresponds to 1,991,903 insured people. Figure 33 shows how that total enrollment is broken down across the insurers represented in the data.

Figure 33. Enrollment in CT consumer report card broken down by insurer.

Source: 2022 CT Consumer Report Card

Figures 34 and 35 respectively display how the total enrollment is split across:

Individual, small group, and large group plans

Individual plans are plans purchased on an individual basis, for example through the federal or a state based Affordable Care Act (ACA) marketplace. In the case at hand, this means plans bought through Connecticut's marketplace, Access Health Connecticut. Group plans are plans administered for a group of employees or other beneficiaries; the term small group has technical meaning that varies by state, but typically refers to employer group health plans for employers with 50 or fewer employees.

Self insured and fully insured plans

Self insured plans are group plans in which premiums are collected by, and covered services for the insured are paid for by, an employer itself. Such plans need not take on the administrative burden of insurance coverage, and often outsource that aspect of insuring to large, well-known insurance companies (often referred to as third party administrators, or TPMs, when they are employed in this role). Fully insured plans are plans purchased by an employer.

Figure 34. Enrollment in CT consumer report card broken down by group type. The data are partitioned according to individual, small group, and large group plans.

Source: 2022 CT Consumer Report Card

Figure 35. Enrollment in CT consumer report card broken down by payer type. The data are partitioned according to fully insured plans and self funded plans.

Source: 2022 CT Consumer Report Card

The data from Connecticut is unique in that it includes a large population of large group health plans, which together with the other data provides for a relatively comprehensive view of the total insured population in the state. It would be invaluable to have such comprehensive data for all states.

Summary of Findings

In studying claims and denials in each of the datasets considered, we've observed a few key points that are consistent across market segments and marketplaces.

- Denials are extremely prevalent, with claims denial rates consistently hovering between 10% and 30%.

- Reporting standards are insufficient to understand the landscape of denials; most denial rationales are recorded as "Other", which is inadequate for understanding how and why denial rates vary across insurers, provider categories, and other partitions of claims.

- Denials pertaining to medical necessity or the experimental nature of treatments comprise a small fraction of all denials, but still account for a large absolute pool of claims denials, and money.

Informed by these findings, we discuss some proposals for improving patient outcomes in the recommendations section below.

Internal Appeals

Next we consider the occurrence of internal appeals in the data. The same datasets that provide information sufficient to compute raw claims denial rates provide information about internal appeals. We again consider these datasets:

- CMS TIC PUFs.

- New York Health Care Claims Reports.

- Connecticut Consumer Report Cards.

- Pennsylvania Department of Insurance Data.

Despite the inconsistencies in reporting across the datasets, the data is striking in that it consistently makes clear that while appeals of all forms are extremely rare among consumers, internal appeal overturn rates are high. We note that this disparity between the fraction of denials being internally appealed and the fraction of those appeals being internally overturned could be rooted in various phenomena12.

Overall Internal Appeal Rates

CMS Federal Marketplace PUFsThe CMS PUFs report the number of internal appeals submitted for denied claims only at the issuer level (so there is not enough information to determine the internal appeal rate for a particular plan).

Analyzing this data is more subtle than it ought to be, because not all issuers in the dataset that report their denial counts report their internal appeals counts, and not all issuers that report their internal appeal counts report their external appeal counts. As a result, simply calculating the ratio of the number of internal appeals reported in the data to the number of denials recorded in the data would only give a lower bound on the internal appeal rate. To address this, we report internal appeal rates by restricting attention to those plans that report both denials and internal appeals.

Among 2021 federal marketplace plans, the average initial appeal rate is about .2%, while the internal appeal overturn rate among this same population of internally appealed claims is about 41%. This data is shown in Figure 36.

Figure 36. Internal appeal rates and appeal overturn rates among federal marketplace issuers in 2021. Only 1/5 of a percent of the approximately 48 million initially denied claims are appealed, but of those that are, 41 percent get overturned on a first level internal review.

Source: CMS TIC PUF data.

The New York Health Care Claims Reports document the number of internal appeals submitted for each insurer in the data. Figure 37 shows the fraction of all initially denied claims that are internally appealed by consumers, and the fraction of those that are overturned on initial appeal. The initial appeal rate is about .6%, while the internal appeal overturn rate among these claims is about 29%.

Figure 37. Internal appeal rates and appeal overturn rates among insurers who submitted health care claims reports to the Department of Financial Services in 2022. Only 1/2 of a percent of the approximately 25 million initially denied claims are appealed, but of those that are, 29 percent get overturned on a first level internal review.

Source: NY Health Care Claims Reports.

The Connecticut Consumer Report Cards document the number of internal appeals submitted for each insurer in the data. Figure 38 shows the fraction of all initially denied claims that are internally appealed by consumers, and the fraction of those that are overturned on initial appeal. The initial appeal rate is about .4%, while the internal appeal overturn rate among these claims is about 60%.

Figure 38. Overall internal appeal rates in the CT consumer report card data. Only .4 percent of the approximately 2 million initially denied claims are appealed, but of those that are, 60 percent get overturned on a first level internal review.

Source: 2022 CT Consumer Report Card

Figure 39 shows the fraction of all initially denied claims that are internally appealed by consumers, and the fraction of those that are overturned on initial appeal in the 2020 and 2021 PA DOI data. The initial appeal rate is about .1%, while the internal appeal overturn rate among these claims is about 59%.

Figure 39. Overall internal appeal rates in the PA DOI data. Only .1 percent of the approximately 3 million initially denied claims are appealed, but of those that are, 59 percent get overturned on a first level internal review.

Internal Appeals by Insurer

As we noted above, each of the datasets provides enough information to compute appeal rates and appeal overturn rates on an individual insurer basis. In what follows we share some such calculations.

CMS Federal Marketplace PUFsFigures 40 and 41 show the internal appeal rates and internal appeal overturn rates for the 10 insurers with the largest volume of claims adjudicated in the 2021 CMS PUF data.

Figure 40. Internal appeal rates for the 10 insurers with the largest number of claims adjudicated in the 2021 federal marketplace data.

Source: CMS TIC PUF data.

Figure 41. Internal appeal overturn rates for the 10 issuers with the largest number of claims adjudicated in the 2021 federal marketplace data.

Source: CMS TIC PUF data.

Figures 42 and 43 show the internal appeal rates and internal appeal overturn rates for the 10 insurers with the largest volume of claims adjudicated in the NY claims report data.

Figure 42. Internal appeal rates for the 10 insurers with the largest number of claims adjudicated in the 2022 Department of Financial Services claims report data.

Source: NY Health Care Claims Reports.

Figure 43. Internal appeal overturn rates for the 10 insurers with the largest number of claims adjudicated in the 2022 Department of Financial Services claims report data.

Source: NY Health Care Claims Reports.

Figures 44 and 45 show the internal appeal rates and internal appeal overturn rates for all insurers in the Connecticut consumer report card data.

Figure 44. Internal appeal rates for insurers in the 2022 Connecticut Consumer Report Card Data.

Source: 2022 CT Consumer Report Card

Figure 45. Internal appeal overturn rates for issuers in the 2022 Connecticut Consumer Report Card Data.

Source: 2022 CT Consumer Report Card

Figures 46 and 47 show the internal appeal rates and internal appeal overturn rates for all insurers in the Pennsylvania Department of Insurance data.

Figure 46. Internal appeal rates for 10 insurers with the most claims in the PA DOI data.

Figure 47. Internal appeal overturn rates for 10 insurers with the most claims in the PA DOI data.

Dataset Specific Considerations

The considerations above exhaust most of the analysis on internal appeals that can be done in a common way across the datasets reporting internal appeal counts. In what follows, we consider a few additional aspects of the data reported in only some of the datasets.

New York Health Care Claims ReportsThe data recorded in the New York Health Care Claims Reports allow us to investigate how internal appeal rates and internal appeal overturn rates vary by provider category. Figure 48 shows the overall claims denial rates, internal appeal rates, and internal appeal overturn rates for each of these categories, aggregated over all insurers in the dataset.

Figure 48. Denial, internal appeal, and internal appeal overturn rates across provider categories in the 2022 New York Health Care Claims Reports.

Source: NY Health Care Claims Reports.

While all provider categories have relatively high internal appeal overturn rates, initial denial rates and internal appeal rates vary widely across the categories. It is noteworthy that while claims for inpatient hospital visits occupy a small fraction of the total claims covered in the dataset (compare Figure 28), denial rates for those claims are high at 24%, and internal appeal rates are two to six times larger than those occurring among the other categories. Despite this increased appeal rate, appeal overturn rates remain high at 27%.

This empirical phenomenon is informed by considering the underlying costs associated with the claims in each of these provider categories. The cost data, displayed in Figure 49, shows that the sum of the allowed amounts for internally appealed 'Inpatient Hospital' claims is greater than the sum for any other category. Moreover, consumers collectively recouped roughly 60% of the entire monetary value of these appealed 'Inpatient Hospital' claims, despite having an appeal overturn rate of only 27%.

Figure 49. Reported total allowed amounts for internally appealed claims, and appeal overturns, broken down by provider category in the 2022 New York Health Care Claims Reports.

Source: NY Health Care Claims Reports.

To summarize, consumer behavior in successfully appealing Hospital Inpatient denials led to the overturn of a very lucrative portion of the internally appealed denials in the dataset; this is a fact that is not visible when solely considering denial or appeal rates, but it is consistent with the intuition that the most expensive contractually inappropriate denials are the ones most likely to be appealed by consumers or their providers.

Another contributing factor that may be driving this phenomenon is that hospitals often have significant resources provisioned to address contractually inappropriate denials. Hospitals routinely have departments dedicated to insurance claims resolution, and pay full time staff to navigate claims submission and appeals pertaining to a wide variety of issues. It is natural to expect that professionals with ample experience navigating appeals, working for organizations whose revenue and patients depend on successful claims resolution, would both appeal more frequently than would individual consumers, and fare better in their appeal overturn rates.

Connecticut Consumer Report CardsThe data recorded in the Connecticut Consumer Report Cards allows one to consider internal appeal rates and internal appeal overturn rates broken down by the rationale provided for the initial denial. This is an incredibly useful lens through which to view the data, and one which is unfortunately unsupported by most of the datasets.

Figures 50 and 51 show the internal appeal rates and internal appeal overturn rates for each denial rationale in the dataset.

Figure 50. Internal appeal rate among the population of claims corresponding to each denial rationale in the 2022 Connecticut Consumer Report Card.

Source: 2022 CT Consumer Report Card

Figure 51. Internal appeal overturn rate among the population of claims corresponding to each denial rationale in the 2022 Connecticut Consumer Report Card.

Source: 2022 CT Consumer Report Card

In this dataset, the internal appeal rate for NMN denials is between 10 to 50 times larger than the appeal rates in all other categories. On the other hand, internal appeal overturn rates for internally appealed NMN denials are among the lowest of all categories.

We note that the high rate of internal appeals for denials whose rationales involve medical necessity, or the purported experimental nature of a treatment or service, has an intuitive potential cause. Medical necessity of particular services or care is not typically made explicit in insurance contracts; instead, broad definitions, which themselves reference literature and other documents, dictate a purported standard by which medical necessity will be determined. Given these definitions are often ambiguous and ill-defined in nature, it makes good sense that cases involving them would be more subtle, and be more likely to be appealed, than clear cut cases.

For example, if a contract explicitly states something is not covered, or a claim is inappropriately submitted and then denied for a member whose coverage had lapsed at the date of service, there is not much ground on which to make an appeal. This same logic explains why the internal appeal overturn rate is 100% for internally appealed claims which were denied purportedly because they were duplicates; whether or not a claim is a duplicate is a clear cut matter of accounting, so any substantiated appeal of a claim denied for being purportedly duplicate is likely to be sound.

Summary of Findings

In studying internal appeals in each of the datasets considered, we've observed a few key points that are consistent across market segments and marketplaces.

- While claims denials occur frequently, internal appeal rates are vanishingly low; this fact remains true across all categories of denial, so far as can be told from the data which reports sufficient detail to make such a determination.

- Among internally appealed claims denials overturn rates are high.

- The monetary value historically recouped in the observed data through internal appeals overturns is large, despite the fact that internal appeals are vanishingly rare.

Informed by these findings, we discuss some proposals for improving patient outcomes in the recommendations section below.

External Appeals

We now turn to external appeals. The datasets that provide information relating to external appeals are:

- CMS TIC PUFs.

- California CDI external appeal database.

- California DMHC external appeal database.

- New York external appeal database.

- Washington external appeal database.

- Pennsylvania Department of Insurance data.

Each of these datasets reports metadata relating to external or independent review of denied claims in a different way. Despite the variations in how the data is reported, the independent sources display at least one consistent result: the population of claims denials which are upheld on internal appeal and then externally appealed are overturned by external review boards at high rates. This is a key fact to take away from these datasets.

This result suggests that internal review processes may not be sufficient for fair or equitable adjudication. If the populations of internal and external reviewers were all perfectly impartial, and shared consistent, repeatable processes for making their determinations, one would expect near perfect agreement between determinations made by the two bodies for the same pool of denied claims.

Instead, we see staggering disagreement in each dataset about which of the externally appealed claims merit overturn. The disagreement cannot conclusively be attributed to faulty or biased internal appeal processes, but it suggests that either internal appeal adjudication is faulty, external appeal adjudication is faulty, or appeal adjudication is too complex to expect a high degree of consistency between any two reviewers, at least for the population of externally appealed claims. The latter explanation appears unlikely given the relatively consistent external overturn rates across all of the different data sources we exhibit, and across many different independent, third party review organizations.

It is possible that if one were to submit all internally appealed claims to third party external review organizations, one would find that among the population of internally appealed claims there would be a high degree of agreement between internal and external reviewers on appropriate determination outcomes. It is of course impossible to surmise what this hypothetical level of agreement would be if the audit were to occur.